Zambia’s Inflation Returns to Target Band Ahead of Schedule, Strengthening the Case for Growth

Bloomberg reports that annual inflation fell to 7.5 per cent in February — inside the Bank of Zambia’s 6–8 per cent target band for the first time in nearly seven years and faster than the central bank’s own projections.

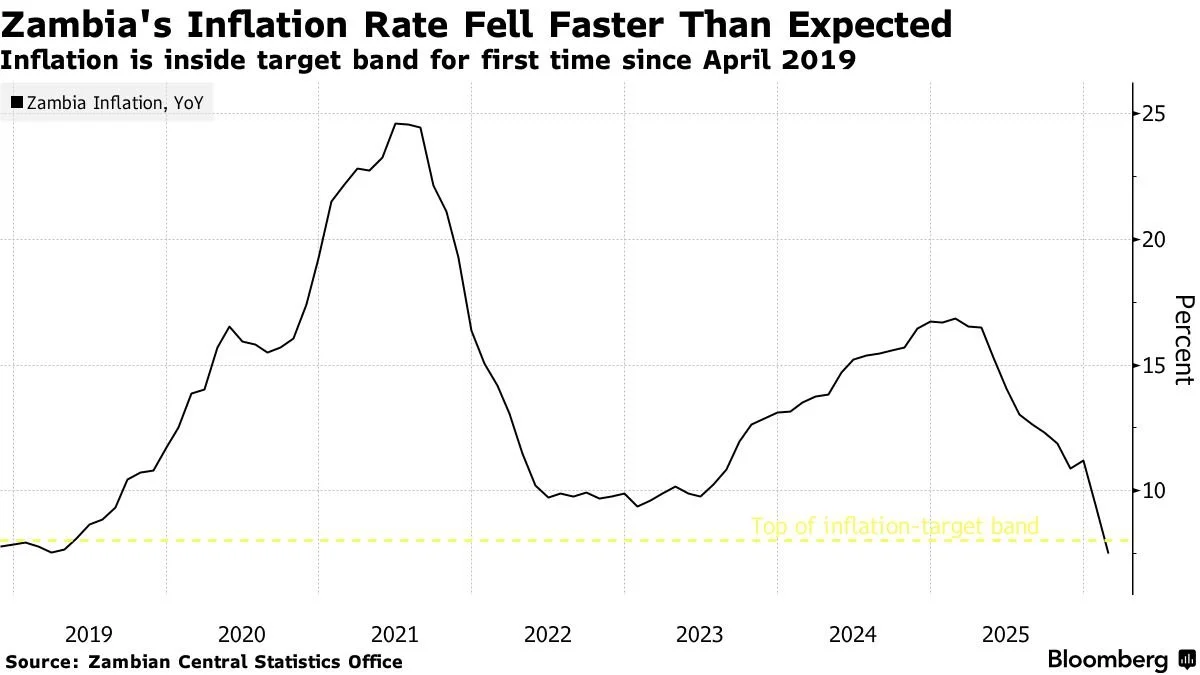

Zambia’s annual inflation rate fell to 7.5 per cent in February, down sharply from 9.4 per cent in January, according to data from the Zambia Statistics Agency reported by Bloomberg. The reading brings inflation inside the Bank of Zambia’s 6–8 per cent target band for the first time since May 2019 — and ahead of the central bank’s own projection, which had anticipated reaching the band by the second quarter of 2026.

For investors tracking Zambia’s macro trajectory, this is a significant milestone. It validates the disinflation path that the Bank of Zambia has been guiding towards and strengthens the case for further monetary easing. The central bank had already delivered a larger-than-expected 75 basis point rate cut on 11 February, lowering the policy rate to 13.5 per cent — a move that surprised markets, where the median expectation had been for a 25 basis point reduction. Governor Denny Kalyalya projected at the time that inflation would average 6.9 per cent in 2026, revised down from a previous forecast of 7.6 per cent, and reach 6.3 per cent in 2027.

Inflation is inside the Bank of Zambia’s 6–8 per cent target band for the first time since May 2019.

The drivers of the decline are broad-based. Food inflation, which carries the heaviest weighting in Zambia’s consumer price index at 54 per cent, cooled to 8.2 per cent from 10.9 per cent, reflecting the ongoing impact of the bumper 2024/25 maize harvest. Non-food inflation softened to 6.5 per cent from 7.3 per cent. On a monthly basis, prices rose just 0.6 per cent, with non-food prices effectively flat. The disinflationary momentum is not coming from a single sector — it is structural, driven by currency strength, improved food supply, and stable energy costs.

The Kwacha’s performance has been central to the story. Zambia’s currency has strengthened more than 17 per cent against the US dollar year-to-date, supported by record copper prices and the central bank’s reinforcement of restrictions on domestic foreign currency use. For dollar-based investors, this currency appreciation has compounded the already attractive nominal yields on Zambian local currency bonds, where recent auctions have cleared at 14–19 per cent.

The broader macroeconomic picture reinforces the signal. Foreign exchange reserves stand at $5.5 billion, providing 4.8 months of import cover. The World Bank’s support portfolio has surpassed $3 billion. GDP growth is projected at 6.4 per cent for 2026 by the government, with the IMF forecasting 5.8 per cent. The fiscal deficit has narrowed from 9 per cent of GDP in 2021 to 2.1 per cent. Zambia never restructured its domestic debt during the 2020 external default, and the government has maintained fiscal consolidation commitments throughout.

The inflation milestone also has practical implications for Zambian consumers and businesses. More than 30 manufacturers have already announced price reductions on essential goods, including mealie meal, sugar and cooking oil, citing improved macroeconomic fundamentals. Lower interest rates, if the easing cycle continues, will reduce borrowing costs for businesses and households — a critical transmission mechanism in an economy where small and medium enterprises account for a significant share of employment.

For the investment case, the February data point matters because it removes a key residual risk from Zambia’s macro narrative. The disinflation has been achieved not through demand suppression but alongside robust growth, rising mining output, and strengthening external balances. That combination — falling inflation, a strong currency, high bond yields, expanding GDP, and improving fiscal metrics — is rare in frontier markets and increasingly difficult for allocators to overlook.

With the next Monetary Policy Committee meeting scheduled for May, markets will be watching whether the faster-than-expected return to the target band opens the door to a further rate cut. Governor Kalyalya has indicated that decisions will continue to be guided by inflation outcomes, forecasts and identified risks. On current trajectory, the data supports continued easing.

Read the full Bloomberg article here.